Client reduces tax bill from Rs 9 lakh to Rs 30,000.

The short version:

With bond funds:

- Taxes only on realised gains

- Income is largely principal, not gains: lower realised gains >>> lower tax

- Inflation protection on realised gains: even lower tax

The long version:

We are helping a retiring CXO plan his retirement.

The client has about 5 crore of investible capital. He has a simple life-style and expects to manage on a budget of 15 lakh a year. He asked us to figure out the best way to generate this as annual income while keeping the capital safe. And he said he prefers fixed deposits.

We crunched some numbers to see what works best: fixed deposits or mutual funds. (Mutual funds that invest in short term AAA bonds — the very safe stuff; as good as fixed deposits.)

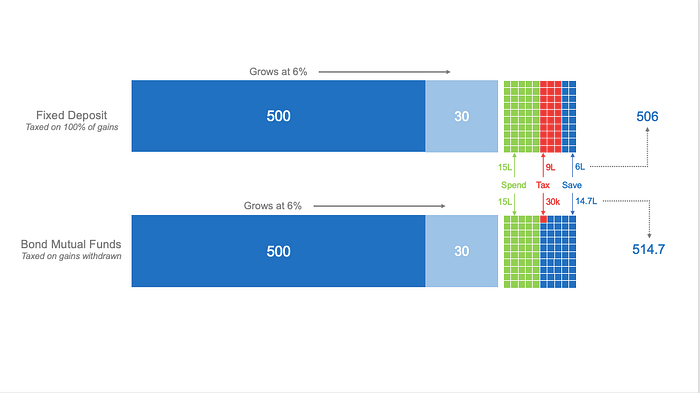

In The Graph Below – Blue Corner: Fixed Deposits

Say the FDs offer 6% interest. That 30 lakh of interest income puts the client in the top income-tax bracket.

Keeping the maths simple (with a single tax bracket and no tax-saving-strategies employed):

- Interest income = 500 X 6% = 30 lakh

- Tax = 30 * 30% = 9 lakh

So he first pays 9 lakh as tax. Then takes out 15 lakh for expenses.

That leaves him with 5.06 crore.

In The Graph Below – Red Corner: Mutual Funds

But if the client were to invest in mutual funds instead, here is how it goes.

Comparing apples-to-apples, say the mutual fund also provides a 6% return. (Unfortunately, bond funds can’t tell you upfront what you will get at the end.)

The client needs 15 lakh for expenses. So he withdraws 15.3 lakh from the mutual fund

- pay 30,000 as tax

- and keep 15 lakh for expenses.

The tax bill went from 9 lakh to 30,000!

How did the tax bill drop? Because of FIFO.

Mutual funds use the FIFO principle: first-in-first-out.

When the client withdraws 15 lakh, about 6% of it is the gain and is taxable. The rest is the principal amount — and therefore not taxable.

Is the client eating into the principal then? Not at all. Here is how FIFO works to the investors’ advantage.

Say an investor invests Rs 100 in a mutual fund. And receives 100 units in the fund (like a share in a company).

The price of each unit is Re 1.

At the end of the year, say the fund gains 10%: the value of the investment is Rs 110.

The price of the unit is now Rs 1.10 per unit.

The investor wants income. So she sells 10 units and receives Rs 11 from the sale.

Of this Rs 11, Rs 10 is the initial investment and not taxable. The gain is Re 1 and this is what gets taxed.

Larger real tax savings

In this case, the taxable income from withdrawing from the mutual fund was Rs 90,000. So the client will likely stay below the taxable income brackets. And effectively, the tax rate is zero.

But if the investor were in the highest income-tax bracket, they would pay tax at a lower rate. This is because mutual funds offer lower tax rates on long-term capital gains.

For bond mutual funds, you need to hold an investment for 3 years to qualify for this lower tax rate.

And the cherry on top is that the gains are first indexed for inflation — just like real estate. So if your return is equal to inflation, you pay no tax. You pay tax only on the bit that is more than inflation.

And that remaining smaller amount is taxed at 20%.

But wait — there’s more.

Now because most of the gain is not taken out, it is not taxed. It stays invested and earns interest on interest — the miracle of compounding at work.

At the end of one year, the bond mutual fund investor will have about 9 lakh more.

In 5 years time: 50 lakh.

In 10 years: a crore and 20 lakh.

If you need help managing your investments, here’s how we think about money.

AutoFi (Autofitech Services Pvt Ltd) is an AMFI-registered Mutual Fund Distributor